The structural factors that have driven the U.S. dollar over the past three years are losing steam: the growth gap between the United States and the rest of the world is narrowing, the U.S. Federal Reserve (Fed) has begun cutting its key interest rates, and the European Central Bank (ECB) may soon raise its own.

These developments point to a weakening of the US dollar in 2026, particularly against the euro and the yen. However, a resilient US stock market could limit the likelihood of this scenario materializing.

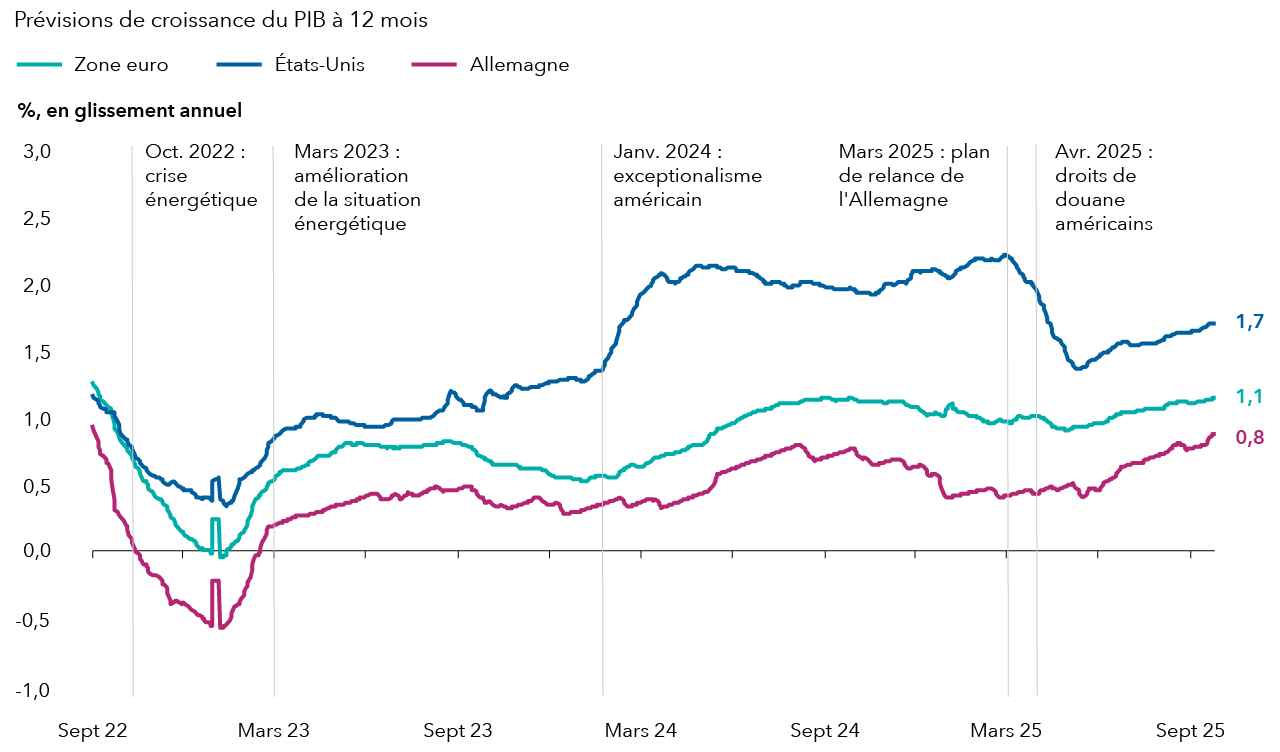

Global growth prospects are aligning with the scenario of a depreciating US dollar

Past performance is not indicative of future results. As of September 25, 2025. Source: calculations by Capital Strategy Research, Bloomberg. Consensus forecasts based on years N and N+1.

In recent years, the U.S. economy has stood out for the resilience of its long-term growth, driven by robust consumption. But recently, several economic indicators have deteriorated slightly in the United States, starting with the nonfarm payrolls data released in early August. In the medium term, uncertainty surrounding U.S. policy, pressures resulting from tariffs, and the slowdown in the labor market could continue to weigh on U.S. growth.

Conversely, the European economy is rebounding: strong activity in the services sector and household consumption are helping to offset the slowdown in manufacturing, and the labor market remains solid across Europe. In this environment, the euro is expected to appreciate against the US dollar as Germany’s fiscal stimulus plan begins to filter through to the real economy, while the yen is expected to benefit from the narrowing of the real interest rate differential with the United States.

Furthermore, the level of the U.S. stock market impacts the valuation of the U.S. dollar: over the past decade, global demand for U.S. stocks—particularly in the technology sector—has been robust, serving as a major factor supporting the greenback. This demand came from investors based in Japan and Europe, markets characterized by stubbornly low interest rates, weak growth, and policies that were not conducive to investment. By comparison, U.S. assets therefore appeared to offer higher returns.

The strength of the U.S. equity market also attracted U.S. investors favoring passive management (such as sovereign wealth funds), which resulted in a decline in capital flows from the United States to emerging economies.

Today, this dynamic could shift. On the one hand, U.S. stocks are trading at exceptionally high valuations, both in absolute terms and relative to their counterparts in the rest of the world, and thus present significant risk. On the other hand, “American exceptionalism” could persist, whether through stock outperformance or a rebound in growth, which could allow the dollar to hold up for some time despite a less favorable global economic environment.

With concerns about the Fed’s independence, the U.S.’s deteriorating budget balance, and the growing “de-dollarization” of international trade, the view that the U.S. dollar is destined for structural weakness is gaining traction.

Nevertheless, the dollar remains the most widely used currency in trade and financial flows, in countries’ foreign exchange reserves, and in corporate reserves of value to protect against periods of economic hardship. Its role within the global financial system should therefore be preserved for the time being, especially since there is currently no viable alternative to the dollar: the euro is not (yet) a safe, unified asset, while the renminbi’s potential is limited by the capital controls implemented by China. Therefore, unless other economies develop sufficiently to become more liquid and deeper capital markets, the dollar should retain its dominant position—and even strengthen it further if certain conditions are met.

In conclusion, while a prolonged decline in the U.S. dollar is possible, it should remain supported by the size of the U.S. economy and financial markets.

Download the full analysis by clicking here.

Other articles by Capital Group are available here.