€4.38 billion. That is the revenue generated by financial investment advisors (CIFs) in 2024, a figure that underscores the economic significance of financial advisory services in an increasingly demanding environment.

This figure comes from the annual overview published by the French Financial Markets Authority (AMF), which compiles quantitative and qualitative data reported by the profession as part of its regulatory reporting. Beyond the numbers, the report reveals a profession in transition, marked by market consolidation, evolving business models, and ever-increasing standards.

Robust revenue, driven by hybrid models

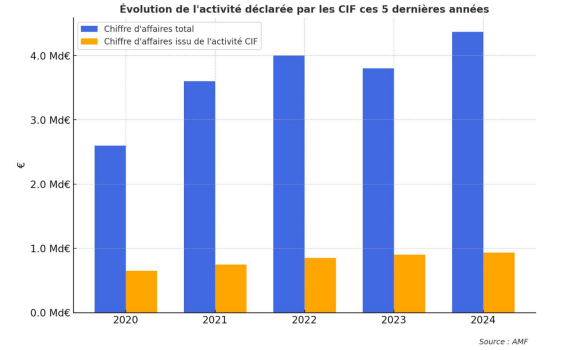

In 2024, CIFs generated €4.38 billion in cumulative revenue, confirming their central role in France’s advisory and investment ecosystem.

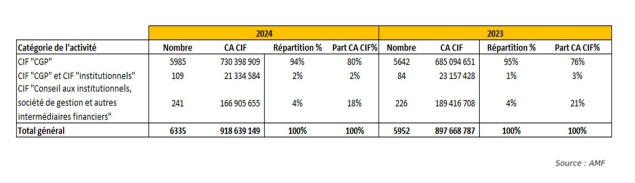

In detail, €918 million came directly from CIF activity in the strict sense, representing approximately 21% of total revenue. This share has declined slightly compared to previous years, when it stood at around 23%.

This trend reflects a fundamental shift: regulated advisory services remain a cornerstone, but are increasingly integrated into comprehensive offerings that combine wealth management, distribution, financial engineering, and strategic client support.

An increasingly concentrated market

In 2024, the top 50 CIFs now account for 50% of total revenue, up from 47% in 2023.

This increased concentration reflects the ability of large firms to absorb regulatory constraints, standardize their processes, and invest in compliance, tools, and teams. Conversely, it exacerbates the challenges for smaller firms, which face growing pressure to reach a critical mass.

The breakdown of revenue by professional association confirms this structure, with ANACOFI-CIF dominating, followed by the CNCGP and then the CNCEF, each embodying distinct dynamics and models.

A broad but highly diverse client base

In 2024, CIFs served 2.37 million clients across all business lines, including 525,478 clients specifically within the CIF business line.

Behind these figures, the study highlights significant disparities in practices.

A minority of players account for a high number of clients and deploy large-scale advisory services, while the majority of CIFs manage smaller portfolios, often with a more personalized and relationship-based approach.

In their recommendations, CIFs continue to favor domestic financial instruments, with a central role given to mutual funds, which remain the foundation of the proposed allocations.

CIFs, CGPs, and Institutional CIFs: Two Economic Logics

The study clearly distinguishes between two major categories of professionals.

- “CGP” CIFs, which make up the vast majority, represent 94% of the market and generate nearly 80% of CIF revenue. Their business is based on a comprehensive approach to wealth management, primarily focused on individuals and business executives.

- Institutional CIFs, though less common (4% of the total), account for approximately 18% of CIF revenue. They handle more complex mandates for institutional investors, asset management firms, and financial intermediaries, offering significant technical expertise.

A Solid Profession, but One Undergoing Transformation

Beyond the numbers, the 2024 outlook reveals a structural shift in the profession.

The CIF remains a pillar of financial advisory services, but its value is shifting: it no longer rests solely on the act of advising, but on the ability to integrate it into a robust, differentiated, and sustainable model.

👉 In a world that is more volatile, more regulated, and more fragmented, these figures call above all for dialogue. At Hubfinance, we are convinced that these challenges are best addressed through peer-to-peer dialogue. Continue the discussion and register for our upcoming Asset & Wealth Management luncheons to debate these issues in complete confidentiality.